Altria (NYSE: MO) is widely known among income-oriented investors for its consistently high dividend yield and iconic brand portfolio. However, in a dynamic regulatory and consumer environment, understanding the company’s investment case requires an integrated view of its income-generating power, competitive strengths, and long-term strategic outlook.

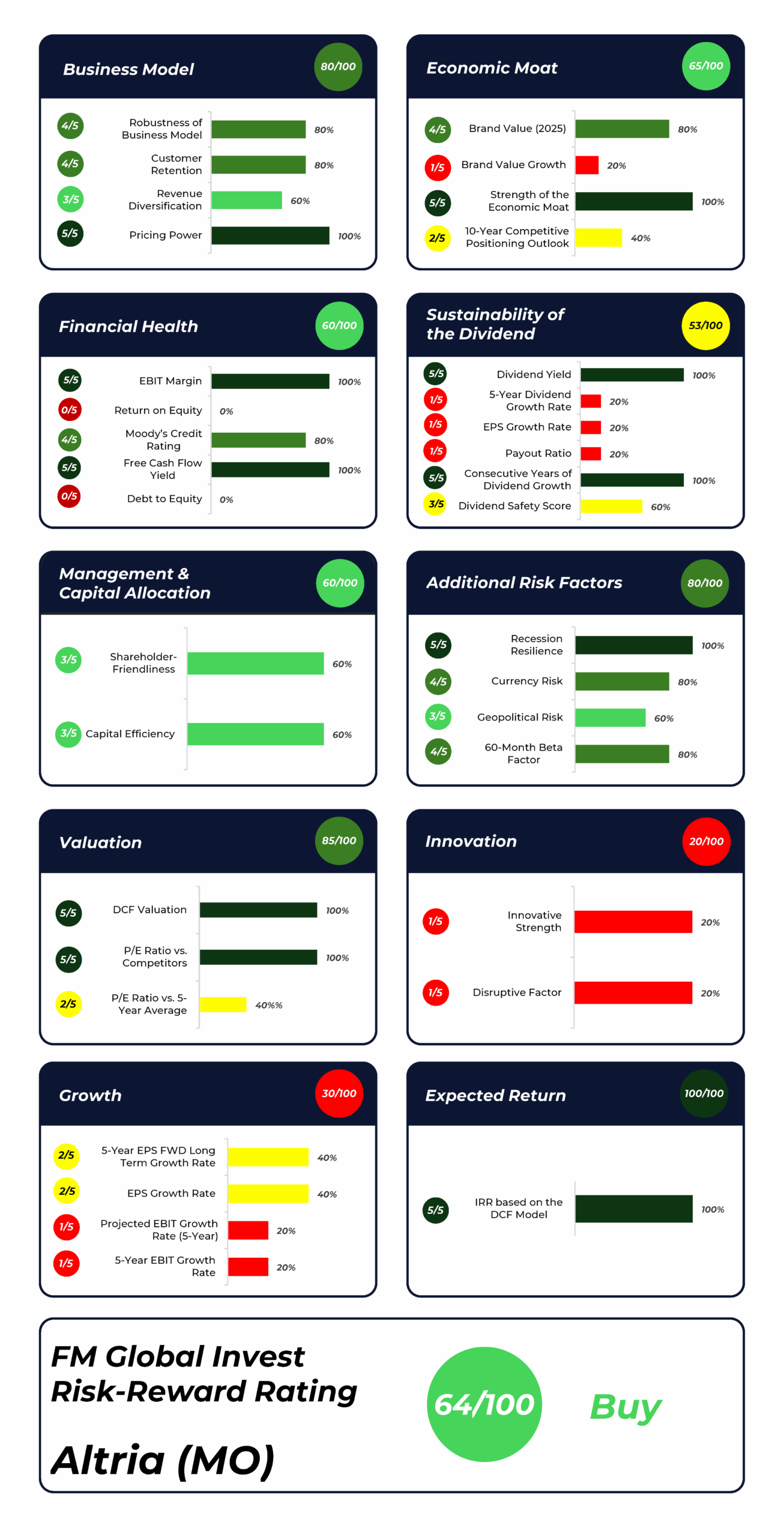

The FM Global Invest Risk-Reward Rating provides a holistic framework for this evaluation. According to our rating system, Altria receives a 64 out of 100 risk-reward score, which implies a Buy Rating for the company.

How Altria Generates Revenue

Altria’s revenue is primarily derived from the sale of tobacco products in the U.S. market.

Smokeable Products

This segment remains Altria’s largest revenue contributor. It includes leading cigarette brands such as Marlboro, which captured 59.3% of the U.S. premium cigarette market in 2024. The segment produced $10.9 billion in adjusted operating companies income (OCI) with a margin of 61.6%, demonstrating robust pricing power despite secular volume declines.

Oral Tobacco Products

Altria’s portfolio also includes smokeless tobacco products through Copenhagen and the nicotine pouch brand on!. In 2024, the oral tobacco segment grew its adjusted OCI by 5.2%, achieving a 67.8% margin—its most profitable business line.

Smoke-Free Innovations

The company is investing heavily in its transformation strategy. NJOY, Altria’s e-vapor brand, expanded distribution to over 100,000 stores and showed volume and market share growth. Helix, the maker of on!, increased shipment volume by over 40% and reached 8.3% of the U.S. oral tobacco category. Heated tobacco initiatives such as Ploom (via the Horizon JV) and the SWIC test launch aim to diversify revenue over the long term.

Equity Investments

Altria maintains a significant stake in Anheuser-Busch InBev. In 2024, it partially monetized this investment to help fund its $3.4 billion share repurchase, enhancing capital flexibility.

Competitive Advantages

Altria’s competitive positioning is supported by several long-term advantages:

Brand Leadership

Marlboro is one of the most valuable and widely recognized cigarette brands in the world, providing Altria with pricing flexibility and durable customer loyalty.

Retail and Distribution Strength

Altria maintains deep retail relationships and premium shelf positioning, critical for visibility and trial generation—particularly as it expands NJOY and on!.

Regulatory Barriers

Strict FDA regulations, while burdensome, create high barriers to entry that benefit established players like Altria. Its regulatory expertise offers a competitive edge in navigating evolving compliance requirements.

Cash Flow Stability

Consistent free cash flow generation allows Altria to sustain generous dividends and execute capital returns even amid market headwinds.

Altria According to the FM Global Invest Risk-Reward Rating

The Evaluation of each Category of Altria based on the FM Global Invest Risk-Reward Rating

Business Model: 80/100

Altria’s business model benefits from strong brand loyalty, high-margin premium positioning, and operational efficiency. Pricing power remains intact despite secular volume declines. While revenue diversification remains moderate, the company has made initial progress in expanding its smoke-free portfolio.

Economic Moat: 65/100

Altria possesses a wide economic moat underpinned by brand power, regulatory protections, and scale advantages. However, its 10-year competitive outlook in a transitioning industry is less certain.

Financial Health: 60/100

The company’s ability to sustain high adjusted operating margins—61.6% in smokeable products and 67.8% in oral tobacco—reflects strong cash flow generation and continued capital discipline.

Dividend Sustainability: 53/100

With a forward yield over 6% and 59 consecutive years of dividend growth, Altria ranks as one of the most reliable dividend payers. However, a 77% payout ratio and limited expected EPS growth (~3–4%) point to slower dividend growth potential in the coming years.

Valuation: 85/100

The company has a P/E (FWD) Ratio of 12.10, well below its peer group. A DCF analysis reveals ~36% upside, making valuation one of the strongest aspects of Altria’s investment thesis.

Innovation: 20/100

Despite expanding NJOY and advancing heated tobacco trials, Altria’s innovation score remains low.

Growth: 30/100

Growth remains subdued across most metrics. EBIT and EPS growth expectations hover between 2% and 4%.

Management & Capital Allocation: 60/100

In 2024, Altria returned over $10.2 billion to shareholders. While current allocation is disciplined, legacy missteps (e.g., JUUL) temper confidence in long-term strategic execution.

Additional Risk Factors: 80/100

Altria exhibits defensive traits—low beta (60-month beta factor of 0.62), U.S.-centric operations, and predictable demand—making it resilient during downturns. However, regulatory and litigation risks remain ever-present.

Expected Return: 100/100

Based on FM Global Invest’s DCF assumptions, Altria offers an upside potential of 35.8%.

Strategic Alignment with The Dividend Income Accelerator Portfolio

Altria exemplifies the characteristics sought in The Dividend Income Accelerator Portfolio: high and stable yield, durable cash flows, and a disciplined capital return strategy. With 55 years of dividend growth and industry-leading margins (smokeables at 61.6%, oral tobacco at 67.8%), Altria’s income reliability stands out. Its pivot toward harm-reduction products like NJOY and on! supports long-term viability and aligns with our emphasis on sustainable income.

Who Should Consider Investing in Altria?

Altria suits income-focused investors—particularly retirees—seeking elevated, consistent dividends with U.S.-centric exposure. Its defensive profile provides portfolio balance, especially in low-growth or volatile markets. However, ESG-focused or growth-oriented investors may find its tobacco exposure less aligned with their investment goals.

Key Risks to Monitor

Key risks include regulatory headwinds, especially from the FDA; competition from illicit e-vapor products; and ongoing litigation. Declining cigarette volumes remain a structural concern, and the company’s high payout ratio limits reinvestment flexibility. Vigilance is required as Altria navigates its smoke-free transition.

Key Investor Takeaways

- Score according to the FM Global Invest Risk-Reward Rating: 64 out of 100

- Rating: Buy

- Suggested Allocation Limit: Up to 3% relative to the overall portfolio

Conclusion

Altria continues to be a foundational holding for dividend-focused investors. The company currently represents 2.13% of The Dividend Income Accelerator Portfolio.

While the company faces innovation and regulatory challenges, its strong brand, pricing power, and shareholder discipline offer a compelling value proposition. Success in transitioning toward reduced-risk products will be key to sustaining income and enhancing total return potential.

For investors prioritizing yield, value, and cash flow dependability, Altria remains a worthy candidate for long-term consideration.

Author’s Note: I have a long term position in Altria.

Sources: Altria’s Annual Report 2024, Morningstar, Seeking Alpha.

Want to learn more about the FM Global Invest Risk-Reward Rating and how it evaluates other companies?

- Here you can find a detailed explanation of the FM Global Invest Risk-Reward Rating.

- Read our latest rating and analysis on Alphabet.

- Here you can find our latest rating and analysis on PepsiCo.

- Explore our latest rating and analysis about Allianz.

- Discover our latest rating and analysis on LVMH.

The FM Global Invest Risk-Reward Rating and how it evaluates ETFs

- Explore the detailed explanation of the FM Global Invest Risk-Reward Rating for ETFs.

- Discover our latest rating and analysis about the Schwab U.S. Dividend Equity ETF.