Alphabet stands as one of the most innovative companies in the world, operating at the intersection of technology, data, and global connectivity. Through its dominant platforms like Google Search, YouTube, Android, and Google Cloud, the company continues to shape the digital economy.

In this comprehensive analysis, we evaluate Alphabet using the FM Global Invest Risk-Reward Rating framework, which assesses companies across multiple dimensions including business model, valuation, innovation, financial health, competitive positioning, and expected return.

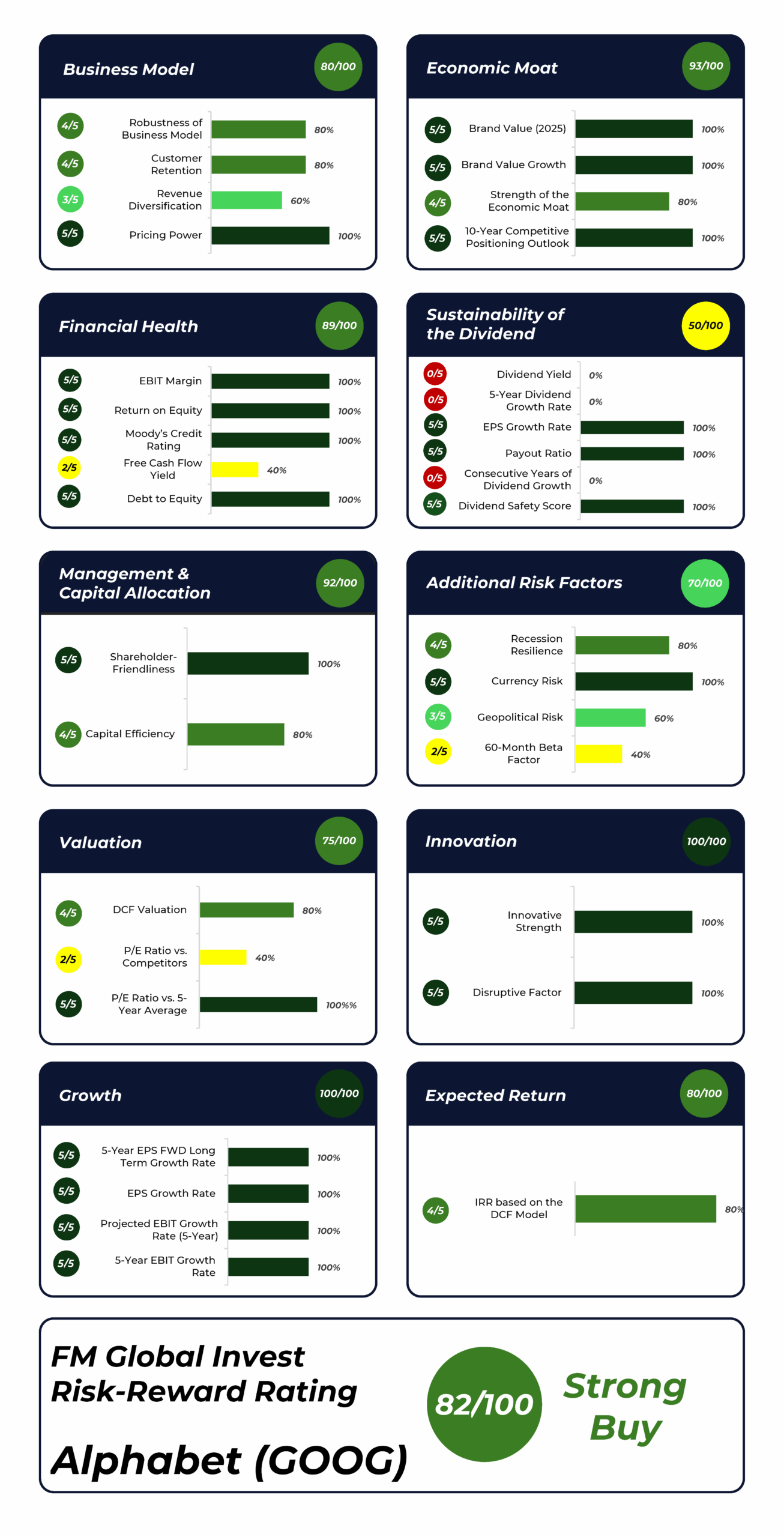

With a total score of 82 out of 100, Alphabet ranks as a highly attractive investment from a risk-reward perspective. Alphabet receives a Strong Buy rating, making it a compelling candidate for long-term investors focused on dividend growth and capital appreciation.

Alphabet scores particularly well in the following categories:

- Innovation: 100 out of 100 score

- Growth: 100 out of 100 score

- Economic Moat: 93 out of 100 score

- Management & Capital Allocation: 92 out of 100 score

How Does Alphabet Generate Revenue?

Google Services

Alphabet’s largest segment, generating over 75% of the company’s total revenue, includes:

- Advertising on Google Search, YouTube, and across the Google Network (performance and brand ads).

- Subscriptions such as YouTube Premium, YouTube TV, and Google One.

- Platform fees from Google Play Store (apps and in-app purchases).

- Hardware sales, including Pixel devices and accessories.

Google Cloud

This segment earns revenue through:

- Google Cloud Platform (GCP): Infrastructure, AI tools, data analytics, and cybersecurity.

- Google Workspace: Productivity tools like Gmail, Docs, and Meet, enhanced by generative AI (Gemini).

Revenue is primarily from subscriptions and usage-based fees.

Other Bets

Alphabet’s portfolio of early-stage, high-risk ventures. Key areas include:

- Waymo (autonomous vehicles)

- Verily (health technology)

Revenue is still limited and mainly comes from healthcare and internet-related services.

Alphabet’s Most Significant Competitive Advantages

1. Scale and Global Reach

Alphabet operates platforms—such as Google Search, YouTube, and Android—that serve billions of users worldwide. This scale creates powerful network effects, supports massive data collection, and enables continuous improvement across its services.

2. Leadership in Artificial Intelligence and Machine Learning

Alphabet has integrated AI and machine learning across its core products and services, including Search, Ads, Cloud, and Workspace. Its Gemini model family and long-standing investment in AI research position it at the forefront of AI innovation and deployment.

3. Diversified and Resilient Revenue Streams

Alphabet generates revenue from a broad range of sources, including digital advertising, cloud services, consumer subscriptions, and hardware. This diversification reduces reliance on any single income stream and enhances overall business resilience.

4. Significant Investment in R&D and Innovation

With nearly $49 billion invested in R&D in 2024, Alphabet demonstrates a strong commitment to technological advancement. This fuels product development across AI, infrastructure, and new ventures, and reinforces its ability to stay ahead of disruptive trends.

5. Integrated Ecosystem of Essential Products

Alphabet offers a tightly connected suite of services—including Gmail, Google Maps, Chrome, YouTube, and Google Drive—which are deeply embedded in users’ daily lives. This integration enhances user retention and strengthens switching costs.

6. Robust Financial Position

Alphabet’s strong cash position and consistent free cash flow generation provide it with the flexibility to invest in growth opportunities, weather economic downturns, and return value to shareholders through share repurchases.

Alphabet According to the FM Global Invest Risk-Reward Rating

Here you can find a detailed explanation of the FM Global Invest Risk-Reward Rating.

Evaluation of Alphabet’s Subcategories Based on the FM Global Invest Risk-Reward Rating

Business Model

Alphabet demonstrates a highly robust and scalable business model, underpinned by a dominant presence across Search, YouTube, Android, and Google Cloud. Its model benefits from strong recurring revenue, massive global reach, and powerful network effects.

Customer Retention

Alphabet’s products—such as Gmail, Google Maps, YouTube, and Chrome—are deeply embedded in users’ daily lives, driving long-term engagement. While many core services are free, user dependency ensures high retention across both consumer and enterprise segments (e.g., Workspace).

Revenue Diversification

While Alphabet is expanding into cloud computing, subscriptions, and hardware, it still derives the majority of its revenue from digital advertising. This creates some concentration risk, although the growth of Google Cloud and YouTube subscriptions is reducing that over time.

Pricing Power

Alphabet possesses exceptional pricing power, particularly in its ad business, where it benefits from unmatched user intent data and targeting capabilities. Its differentiated AI-powered solutions further enhance monetization efficiency across platforms.

Overall, Alphabet scores 80 out of 100 in the Business Model category, reflecting a business model that is structurally sound, highly profitable, and positioned for durable competitive advantage—despite reliance on advertising revenues.

Economic Moat

- Strong global brand: With a brand value of $413B, Google is presently the third most valuable brand in the world, according to Brand Finance.

- Increasing brand value: Compared to the previous year, Google’s brand value has increased by 24%.

- The probability that Alphabet will maintain its leading position within the Interactive Media and Services Industry is very high.

Financial Health

- Alphabet’s EBIT Margin of 33.17% is an indicator of the company’s excellent position within the Interactive Media and Services Industry.

- Alphabet’s Return on Equity of 34.79% reflects strong capital efficiency.

- The company’s Aa2 credit rating from Moody’s indicates a very low credit risk, which is in line with our objective to preserve capital above all.

- Alphabet’s low Total Debt to Equity Ratio of 8.25% indicates a low financial leverage.

Sustainability of the Dividend

- Alphabet’s low Payout Ratio of 11.15% suggests plenty of room for dividend enhancements in the years ahead.

- The same is indicated by Alphabet’s relatively high EPS Growth Rate of 20.76%, which shows that the company can continue increasing its earnings per share and supports strong dividend sustainability.

Management and Capital Allocation

In the Shareholder Friendliness subcategory Alphabet receives a 5 out of 5 score while it receives a 4 out of 5 score in the Capital Efficiency subcategory.

Additional Risk-Factors

Alphabet shows strong resilience in key risk areas. Its global diversification and recurring revenue streams support solid performance during economic slowdowns. However, the company remains exposed to regulatory and geopolitical developments and displays slightly elevated market volatility, which leads to a 70 out of 100 score in the Additional Risk-Factors Category.

Valuation

Based on the Valuation of our DCF Model, Alphabet presently has an Upside potential of 18.2%, indicating that the company is presently undervalued. The same is indicated when having a look at Alphabet’s P/E (FWD) Ratio of 19.03, which stands 22.79% below the Sector Median.

Innovation

In the Innovation Strength and Disruptive Factor subcategories, Alphabet receives the highest possible 5 out of 5 rating, resulting in a 100 out of 100 rating in the Innovation Category.

The reason for Alphabet’s high ratings in this category are its industry-leading investments in artificial intelligence and machine learning, its pioneering role in foundational AI technologies (such as the transformer architecture), the consistent integration of cutting-edge innovations across its product ecosystem (including Search, Gmail, YouTube, and Google Cloud), and its ambitious long-term projects like Waymo and Verily that reflect a culture of bold, forward-thinking disruption.

Growth

In terms of Growth, Alphabet reaches the highest possible Rating, which is, among other factors, a result of the company’s high EPS Growth Rate (FWD) of 20.76% and its high 5-Year Average EBIT (YoY) Growth Rate of 30.32%.

Expected Return

At Alphabet’s current share price, our DCF Model indicates an Internal Rate of Return of 13.58%, leading to a 4 out of 5 score in the Expected Return Category.

Strategic Alignment with The Dividend Income Accelerator Portfolio

I see Alphabet as an important position to enhance the dividend growth potential of The Dividend Income Accelerator Portfolio. Due to Alphabet’s low Payout Ratio and high earnings per share growth rates, in addition to the company’s significant competitive advantages, the company is well-positioned to significantly increase its dividend in the coming years.

Who Should Consider Investing in Alphabet?

- Investors who prioritize dividend growth and capital appreciation.

- Investors who want to benefit from Alphabet’s attractive risk-reward profile, enabling investors to achieve an attractive Total Return.

Key Risks to Monitor

1. Regulatory and Legal Risks

Alphabet faces increasing global scrutiny related to antitrust, privacy, and content moderation, which could lead to costly compliance measures, fines, or limitations on business practices.

2. Data Privacy and Security Risks

Growing global data protection laws and the risk of data breaches may restrict Alphabet’s ability to use personal data effectively and could harm its reputation and financial standing.

3. Competitive Pressure

Alphabet competes in highly dynamic markets against major players like Amazon, Microsoft, Meta, and new AI entrants, and must innovate continuously to maintain its leadership.

4. Heavy Reliance on Advertising Revenue

A large portion of Alphabet’s revenue comes from digital ads, making it vulnerable to economic downturns, changes in advertiser spending, and evolving ad regulations.

5. Artificial Intelligence Risks

The rapid development and deployment of AI may lead to ethical, regulatory, or societal challenges, and any missteps could impact user trust or provoke stricter regulation.

Key Investor Takeaways

- Score according to the FM Global Invest Risk-Reward Rating: 82 out of 100

- Rating: Strong Buy

- Suggested Allocation Limit: Up to 5% relative to the overall portfolio

- Positioning: Ideal for investors who prioritize dividend growth and capital appreciation.

- Valuation: According to different Valuation methods, Alphabet is presently undervalued.

Conclusion

Alphabet’s score of 82 out of 100 based on the FM Global Invest Risk-Reward Rating reflects the company’s exceptional positioning across innovation, growth, capital allocation, and business model strength.

Backed by industry-leading AI capabilities, robust financial health, and a diversified ecosystem of revenue streams, Alphabet is well-equipped to deliver sustainable shareholder value.

While regulatory and market risks persist, its long-term potential makes it a core candidate for portfolios seeking a blend of dividend growth and capital appreciation.

For investors aligned with the strategy of The Dividend Income Accelerator Portfolio, our actively managed dividend portfolio that blends income and growth, Alphabet offers both defensive resilience and forward-looking upside.

Author’s Note: I have a long term position in Alphabet.

Sources: Alphabet’s Annual Report 2025, Morningstar, Seeking Alpha.

Want to learn more about the FM Global Invest Risk-Reward Rating and how it evaluates other companies?

- Here you can find a detailed explanation of the FM Global Invest Risk-Reward Rating.

- Explore our latest rating and analysis about Allianz.

- Discover our latest rating and analysis on LVMH.

The FM Global Invest Risk-Reward Rating and how it evaluates ETFs

- Explore the detailed explanation of the FM Global Invest Risk-Reward Rating for ETFs.

- Discover our latest rating and analysis about the Schwab U.S. Dividend Equity ETF.